The looming financial crisis and the news that keeps emerging is getting so bad that it’s growing harder for me to set aside my rage and discuss it coherently.

But I’m going to try.

I’ll continue to use the framework of the credit cycle, as I hope y’all have been able to digest it. That said there are some events that are happening outside of a normal cycle, not unpredictable, but defintely wild cards and spoilers; chief among them would be the closure of the Straits of Hormuz and its cascading effects on the by-products from gasoline refining. This will lead to a commodity price spike everywhere.

I noted nearly two weeks ago, “The end of this credit cycle is going to include the following macro events: a credit crisis, a housing crisis, an energy shock, with the potential for . . . famine on a biblical scale [in the developing world], at least one Too Big To Fail failing, as Lehman Bros and AIG did in 2008, and the AI bubble bust.”

We are very deep into phase 2 of the credit cycle. We are closer to the end than we are the beginning.

By way of not so new but newly disclosed developments FDIC insured banks are exposed to private credit and/or equity to the tune of $1.4 trillion.

That makes up 11% of total FDIC insured bank lending. This is why I call private credit, shadow credit. And that shadow credit is money that you, dear taxpayer, are on the hook for when the excrement hits the fan.

Moreover, the private credit/equity crisis is much, much worse than I initially thought. I went full Alice down the rabbit hole this weekend. Never in my wildest dreams might I envision the inept deployment of so much capital in so many catastrophically stupid ways.

Here’s that canary, Blue Owl, I’ve been talking about. It’s getting worse for them. Much, much worse: there is a term for 41% redemption demands: a run on the mother-fucking bank. Blue Owl–as I have mentioned many times before–is linked at the hip with Oracle and its hyperscaling of datacenters. Oracle is trying to back door a Federal backstop, justifying it as a necessary AI upgrade to Fed databases, which is bullshit, but it might work.

Fun fact: all planned data-centers for 2026 are either delayed or cancelled. But we’ll get to that later.

The real problem right now is the dilemma, of which I already spoke, facing central bankers from the ECB, Japan and the Fed. I’ll spell it out again.

First, they are facing an inflationary energy shock. They are staring at commodity prices rising coupled with higher inflation expectations from consumers. Inflation is likely to jump. This places enormous pressure on central bankers to tighten credit by raising interest rates.

On the other side of the dilemma is the growing realization, at least I hope they are aware, of just how bad a credit crisis we’re waltzing into.

Housing is in free-fall, too.

The employment numbers are a joke. Sure, the BLS reported 178,000 non-farm payroll jobs added in March. Unemployment fell a bit as well. Except, the way the BLS calculates unemployment is a farce. Consider that 400,000 people exited the labor force during the same month. How does that translate into job growth? (Hint: it doesn’t.)

Unemployment is calculated using U3, meaning people who are actively seeking work and have done so in the past four weeks. A more meaningful, but politically inexpedient measure is U6. U6 “includes U-3, plus discouraged workers, those marginally attached to the workforce, and people working part-time who want full-time work.”

See where I’m going with this?

At the same time BLS was championing these great numbers, they issued an under-the-table revision of the February numbers downwards -133,000. Yup, you read that correctly. Add all the downward revisions over the last two years and employment numbers have cratered downwards to the tune of millions.

Millions.

All this data gives the Fed a bad case of whiplash: raise rates in fear of inflation or lower them, anticipating a credit crisis?

Should I stay or should I go?

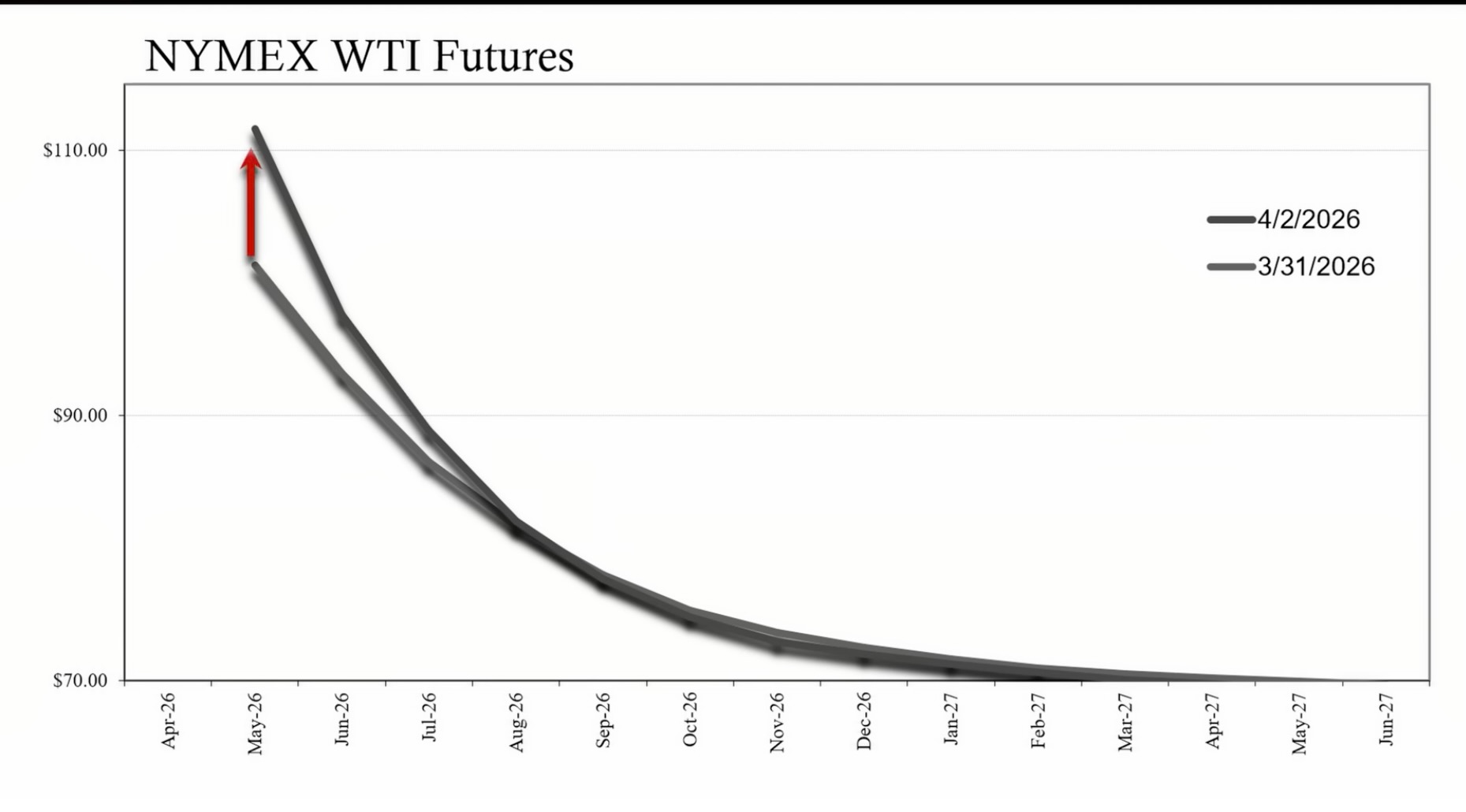

Here’s the kicker that magnifies this dilemma: the signal WTI long-term futures (and treasuries and TIPS) are giving off. Take a look at this chart of WTI:

You can clearly see the near term spike. That’s the inflationary pressure central bankers are worrying about. Brent Crude is even uglier at $140. So, at present WTI is at $111 for April 2026 contracts. But take a look at the futures a year later. The chart doesn’t go that low, but the futures are priced at below $60 a barrel. That’s a $51 spread.

WTI long term futures are predicting serious oil demand destruction over the next 12-months and longer.

What, say you, is demand destruction?

Demand destruction happens when shrinking economic activity across the board globally reduces the need for energy. US Treasuries and TIPS are signaling identical developments.

Shorter version: less economic activity globally means less demand for oil. But my bet is that central bankers will raise rates at first, only to realize the trap they fell into.

Anyone want to take the over/under?

So what does this all mean? Well, EndGameMacro succinctly describes how bad it will probably get: “Unemployment rises roughly 5.5 points to a peak near 10%, equities fall roughly 55% to 58%, home prices drop about 30%, and commercial real estate takes a 39% to 40% hit.”

Personally, I think it’ll get worse. The size of the private equity/credit catastrophe has me questioning whether the Fed can really backstop a crisis this time around, especially when you add the massively irresponsible budget just proposed by Trump.

Finally, a quick word on AI: this post just confirmed my hunch that the AI craze is nothing more than a huge ponzi-scheme and will never truly amound to a hill of beans. Here is a taste of the post:

“So it is with great regret that I announce that the next person to talk about rolling out AI is going to receive a complimentary chiropractic adjustment in the style of Dr. Bourne, i.e, I am going to fucking break your neck. I am truly, deeply, sorry.“

Give it a read. You’ll enjoy it and learn a lot.

What’s it all mean?

Easy, our elites are strip-mining our economy while we’re too busy fucking around on Tik-Tok to care.

ProNewerDeal

“Unemployment rises roughly 5.5 points to a peak near 10%, equities fall roughly 55% to 58%, home prices drop about 30%, and commercial real estate takes a 39% to 40% hit”

Some questions

1 Assuming that this is the trough of price decline, what is the timing of this trough? Sometime between 2026-Jul & 2028-Jan?

2 If this crisis has inflation followed by deflation, what is the peak of CPI during the inflation & the trough of CPI during deflation?

3 What will the reserve currency “market share” be of the top 2 reserve currencies and gold after this crisis? Wikipedia stating in 2025 USD is at 57%, EUR at 20%. Gold is not listed in the “reserve currency market” but in my view it should be.

4 equities here is US stock? What would you guesstimate for ex-US developed stock, & emerging stock? Emerging stock crashed harder than US in 2008. However US stock is among the most expensive in the world based on metrics like Shiller 10-yr PE, whereas many emerging stock is inexpensive.

5 What about 30-yr US Treasuries, gold, & silver?

spud

i predicted that the powers to be, hoped that oil would be turned off by the iranian war. thus making their own oil far more valuable.

Keen agrees with me,

https://www.youtube.com/shorts/xP-8CQdYkFY

its why capitalism must be done away with. the stock markets behavior, tells the story. in the real world, the so-called investors, would have headed for the door by 2024.

the really smart, would have headed for the doors in 1993 if they were alive and mature then. making sure they could survive, once the inevitable hits the fan.

spud

ProNewerDeal:

Gold is not listed in the “reserve currency market” but in my view it should be.

never should gold be considered the same as cash. gold is a store of value, depending on others view of what its worth, and cannot be used in place of cash. it must be sold and converted into cash.

gold is critical in the manufacturing process, and that includes jewelry.

lincoln understood this well, he created the greenback system, and in my opinion, its why he was assassinated, most likely backed by wall street and the banks.

the minute you make gold the same as cash, you invite massive debilitating deflation, even worse than any dim witted neo-liberal/conservative/libertarian could ever accomplish.

if countries use gold as a settlement in trade, both sides will help set off a mass extinction event, unparalleled in modern history.

use currency swaps, a basket of currencies, even out right barter.

StewartM

Easy, our elites are strip-mining our economy…

Started 45 years ago. It’s not news; we’re just seeing the inevitable outcome.

In 1981 (and to some extent, before) the US economy took up smoking. Hey, smoking give you a boost; it may even make you more productive. Those cigarettes look sophisticated, now don’t they? And if you’re a woman, you now can smoke like a man; if you’re a man, you’re now a cowboy!

Of course, as most smokers end up realizing, decades later, it was a very bad decision. Oh there’s those pointy-headed intellectuals called “doctors” who tried to warn you, but who listens to pointy-heads?

Maybe even now, the problems could be fixed. But like the addicted smoker, smoking through the hole in his windpipe they cut for his/her cancer, old habits die hard.

ProNewerDeal

Spud “never should gold be considered the same as cash”. I did NOT say that. I said “Gold is not listed in the “reserve currency market share”, & in my view it should be considered. Or also publish a new 2nd metric “reserve currency + precious metals market share”.

There have been reports Central Banks including China have been increasing gold reserves. I could see a hypothetical & possible scenario where on an aggregately Central Banks sell 20% of their US & Euro Bonds, increase gold, and reserve currency market share “increases” of the USD from 58% to 59%, EUR from 20% to 21%.

Excluding gold obsures what is actually occurring with Central Bank reserves.