For the first time in this Credit Cycle more money is leaving private credit than is going in.

In Q1 2026, $7 billion left non-publicly traded BDCs (business development companies, ie. private credit shops) while they only raised about $5 billion. Total redemption requests from investors to private credit shops topped $15 billion.

Okay class, a little math. If $7 billion was cashed out, only $5 billion was raised then $8 billion of redemption demands were denied investors. That means investors were denied 53% of their redemption requests. (One might call that a run on the bank.)

Systemic Deterioration

We’re talking about the entire private credit industry, here. Not just a bad loan or failing borrower. It’s becoming systemic.

“If there were no war,” as Herr Tarman at Deutschbank said, “in the Persian Gulf this would be dominating the news cycle.”

What makes this very, very bad is when more money leaves the private credit system, sales are forced.

These are not voluntary sales or trades. They are forced, essentially they are margin calls, except, as Bloomberg pointed out, some sales sell for .98¢ on the $1, others sell for .90¢, but one forced sale went real bad for the private credit firm. They got .65¢ on the $1.

That’s a 35% loss. I can recover from a 15% loss but losing 35%? Nope. That’s a busted investment I’m never getting my principal back on. This activity has a name, one rarely uttered on Wall Street, as it is the market equivalent of screaming, “Voldemort,” on the floor of the NYSE.

This is what we in the business call “Accelerating Downside Price Discovery.” (Honestly, last time this happened was in 2008 and I got giddy. I love seeing fools lose boatloads of money. The schadenfreude works like an aphrodisiac on me!)

Accelerating downside price discovery creates a vicious downward cycle in credit markets and later in equity markets. Assets devalue. Private credit shops announce bankruptcy. Lots of people lose jobs.

Then equities decline, soon the investment (Morgan Stanley and Goldman Sachs) and commercial (JPM Morgan Chase, BoA and Wells Fargo) banks crater. In February 2009 I bought an enormous amount of Bank of America at $6 a share. A month later it was trading at $3.50-ish. I was biting my fingernails for sure. But, ten years later I sold it for almost $30 a share. But for ten years the stock traded sideways. So did the equity markets. The Fed’s QE–quantitative easing–made money virtually free and no one paid a price for the sub-prime fiasco.

This time will be different. No one understands what private credit does, except buy up empty houses and make the housing crisis worse.

Petroleum And Economywide Demand Destruction

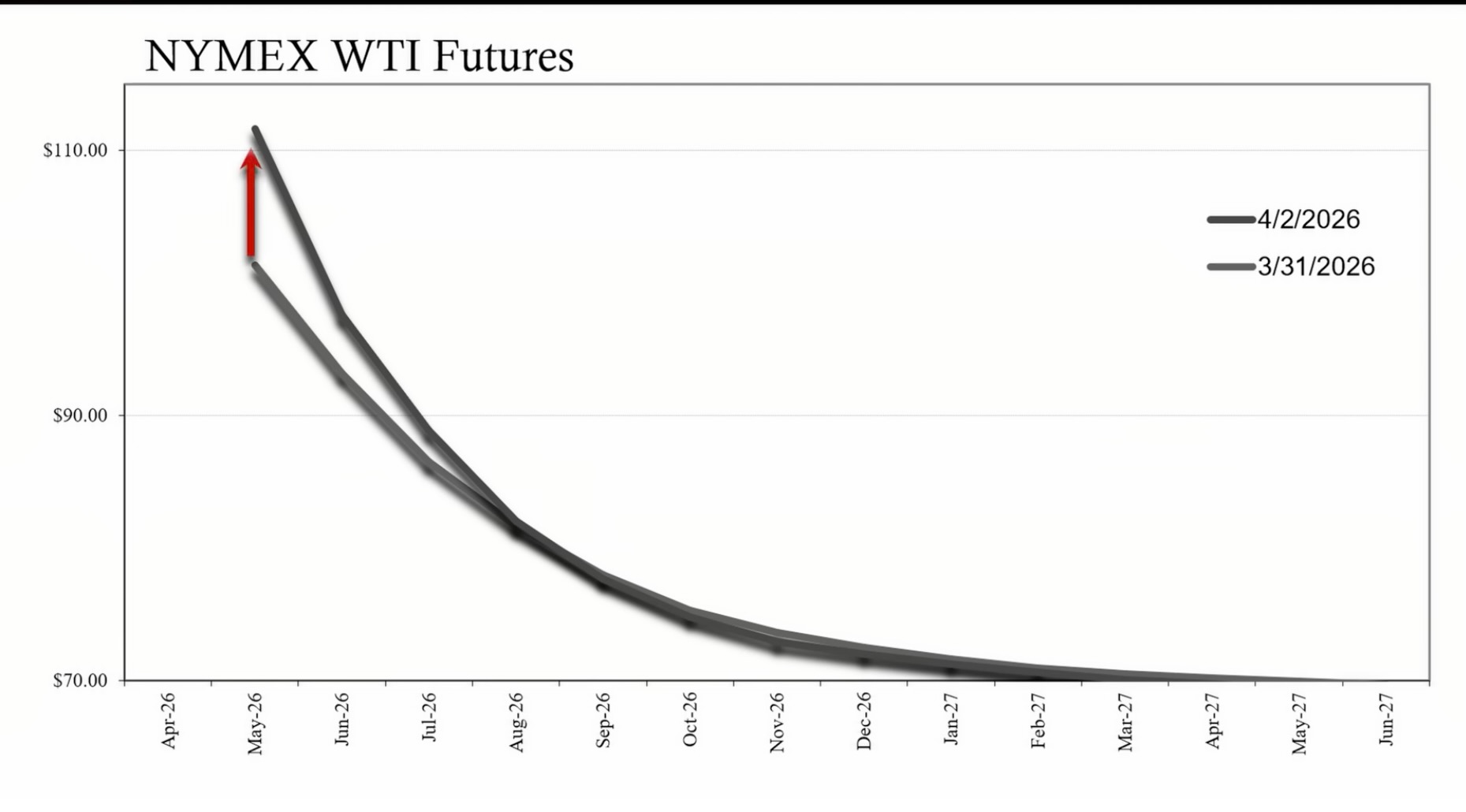

Another consequence: This credit cycle is ending and oil futures are flashing a clear deflationary spiral. This is why I keep pointing out the long end of the WTI Oil futures price contracts going out a year. Here is why oil matters:

In Mid-August US petroleum reserves (non SPR) will fall to 390 million barrels. Today that number is 440mln barrels.

For refineries, pipelines, storage tanks, and terminals to function the system needs a minimum of 380mln barrels in reserve. If reserves fall below that level getting petrol from point A to B is like pushing a string, instead of pumping a viscous liquid.

Let’s do some simple math. We export 5mln barrels a week, plus or minus a million. The US uses 120million barrels a week. Subtract our exports over the next ten weeks. That’s 5×10=50 mln barrels pulled out of the reserve. Subtract 50 mln barrels from present reservers (non SPR) gets us within the margin of error at 390mln barrels. At this rate US petroleum and gasoline reserves will be at crisis levels in mid-August.

And herein lies the big rub, the dilemma of dilemmas, caught between Scylla and Charybdis: how can the Fed backstop a credit crisis with easy credit (because only easy credit solves a credit crisis) when its fighting phantom inflation with high rates, ie. tight credit? It cannot do both. Picture clearing up now?

I’ve been explaining the imminent unraveling of this credit crisis here at Ian’s for at least two months now. Today we’re closer to the end of Phase Two of the Credit Cycle now than we are to its start. When Phase Two unravels fully, that’s when the AI bubble goes pop.

When will that be?

Sooner than we want, but not as quickly as we fear.

“Cowboy up,” folks, as we say down here in Texas, “you’re going to need a raincoat.”