A friend pointed out to me that Israel’s support is eroding hard. The elite consensus is shifting. Point in case:

Israeli National Security Minister Ben Gvir, an anti-Arab racist zealot, says “all of Lebanon must burn.” That’s almost 6 million people. Hideous. https://t.co/ONlrB9jpjo

— Jake Tapper 🦅 (@jaketapper) June 19, 2026

The hard core Zionists will keep opposing this deal, of course, but there are two groups that are shiftable. The first is the one that Tapper belongs to: he’s an authority follower. He’s been hardcore pro-Israel and loathes Muslims, but his first instinct is to follow the leader. Trump’s made a clear turn, and Jake is following.

The second group are those who need administrative favor. Their livelihood or plans depend on the levers the President controls favoring them. They were for Iraq, for Ukraine, etc… but they have no strong ideological commitment, only self-interest.

Trump made a mistake letting hard core Zionists roll up media and social media, but there’s still enough run by self-interested or follow the leader types that if Trump stays solid, the American elite zeitgeist will shift towards his stance. Israel is an ideological commitment, it’s not, for most elites and courtiers, all that involved with making lots of money or being part of the in-group. If the window shifts, they’ll shift with it.

At a fundamental level what happened is that America got itself involved in a war which it couldn’t just walk away from. Losing in Vietnam was embarrassing but really, who cares? Just walk away. Losing in Afghanistan, likewise.

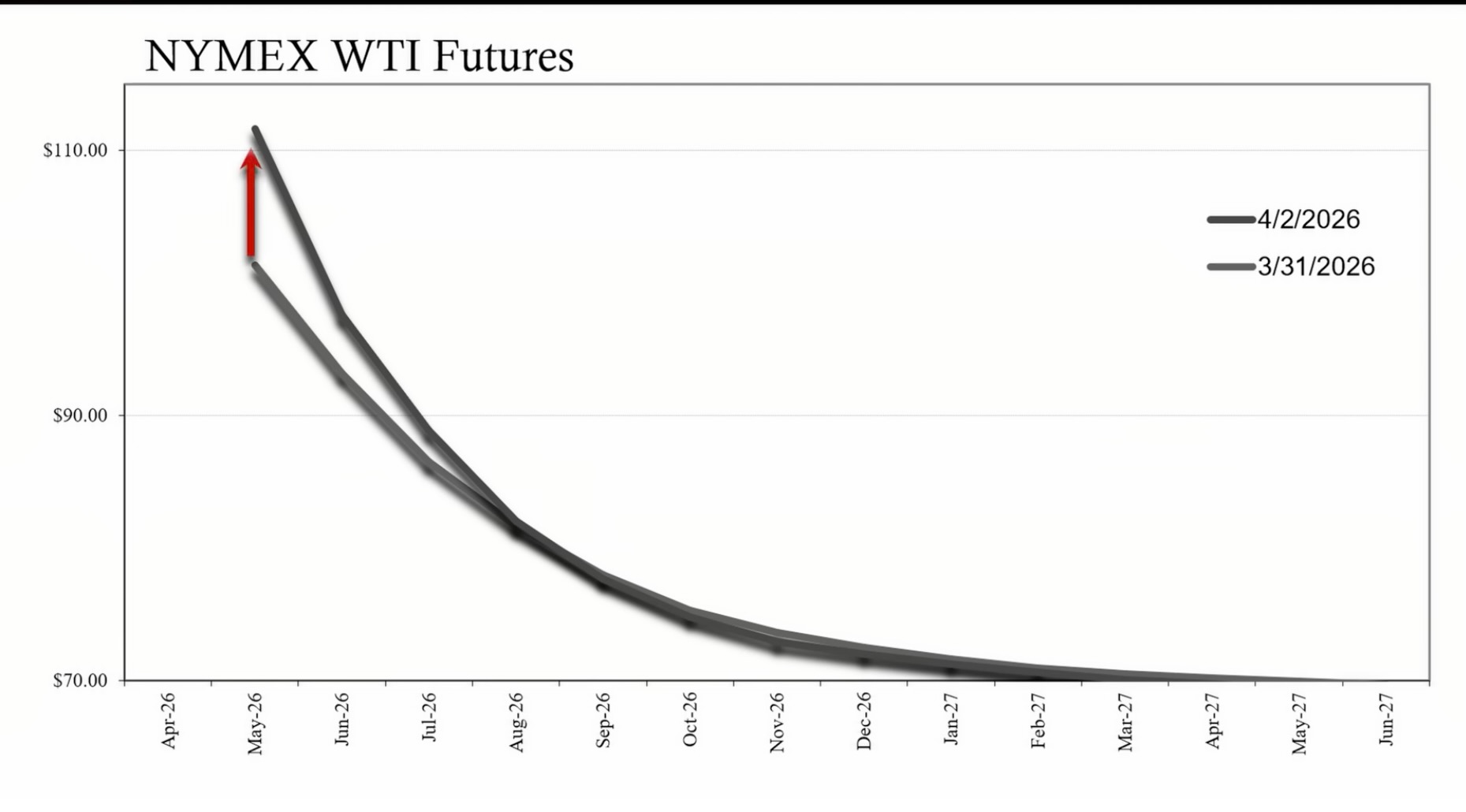

But the Iranians have the West’s balls in a vise and the vise was slowly tightening. Key reserves were way down. Oil at Cushing OK is near historic lows. Distillates are getting scarce. Market manipulation of the price of oil was very successful, but actual physical shortages were on the way, starting in a month or so. (Ironically, price manipulation meant that oil reserves drew down faster than if actual price discovery had been allowed.)

There is a real world, and a real economy and Iran had control of it. The econo-morons talking about how the effect of this has been less than the oil shocks are right when looking at market numbers, but it wasn’t going to stay less and even Trump figured that out.

So the neocons and the hard Zionists will attack, but if Trump had the least concern for the actual economy, he had to make a choice.

Meanwhile Israel is still fighting in Lebanon and the first real battle of the Lebanese invasion is taking place.

The situation on Ali Taher hill and its outskirts right now:

It is outstanding how the resistance heroes, after all Israeli terror and devastating attacks for about 3 years, were able to repel the invasion of the “5th most powerful army in tge world”.

If something can be used to… pic.twitter.com/Q4Gh0Gx5NE— Hadi Hoteit | هادي حطيط (@HadiHtt) June 19, 2026

Both Hezbollah and Israel are concerned there’ll be a new, actually real ceasefire and Israel is seeking to create facts on the ground. Ali Taher hill is an important strategic objective, giving whoever controls it sight lines for miles around. This is the first large engagement I’m aware of in this invasion where Hezbollah has chosen to stand and fight, instead hitting and fading. (That’s not a criticism. Guerilla warfare makes sense for them.)

And so far they’re doing well, because the Israeli ground forces are actually crap.

The Iranians have not gone to Geneva for the signing or negotiations. They are holding firm on Lebanon. And that means Trump can either rein in the Israelis or the vise starts tightening around America’s balls again.

America cannot win this war. It is impossible. Even using nukes probably wouldn’t work fast enough. That’s why they agreed to a deal that is very pro-Iranian.

That has not changed. They can rein in Israel or cut it loose now, or they can do it in two months when the US is in much more pain, or in 4 months when there are food riots.

There’s a real world. America lost a war that matters. There’s going to be a price for that. If America is smart and not completely controlled by Israel, they’ll pay that price now and if necessary cut Israel lose, because the price will go up every day if the MOU fails.

What I write here is for the benefit of everyone, but alas, I live in capitalism and I, and the site, take money to keep running. If you value the writing here and can, please subscribe or donate.

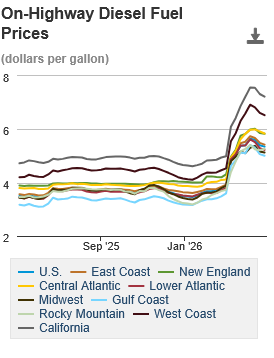

Most farmers use tractors. Most tractors use diesel, and those prices are rising too. They will continue to rise because the oil which is being restricted is the best oil for creating distillates like diesel, bunker fuel (ships) and jet fuel.

Most farmers use tractors. Most tractors use diesel, and those prices are rising too. They will continue to rise because the oil which is being restricted is the best oil for creating distillates like diesel, bunker fuel (ships) and jet fuel.