If you’ve been following oil prices since the Iran war started you’ve probably been surprised at how low prices have often been. I certainly was, at first.

The issue is fairly simple: most governments are worried about the price of oil, and not the supply of oil. So they’ve taken various measures to keep prices low. Some of those have been manipulative financial and some of them have been massive releases of oil from reserves.

IEA chief Fatih Birol told Bloomberg that a historic 400-million-barrel emergency release, equal to roughly 2.5 million barrels a day, helped push oil prices down by $20.

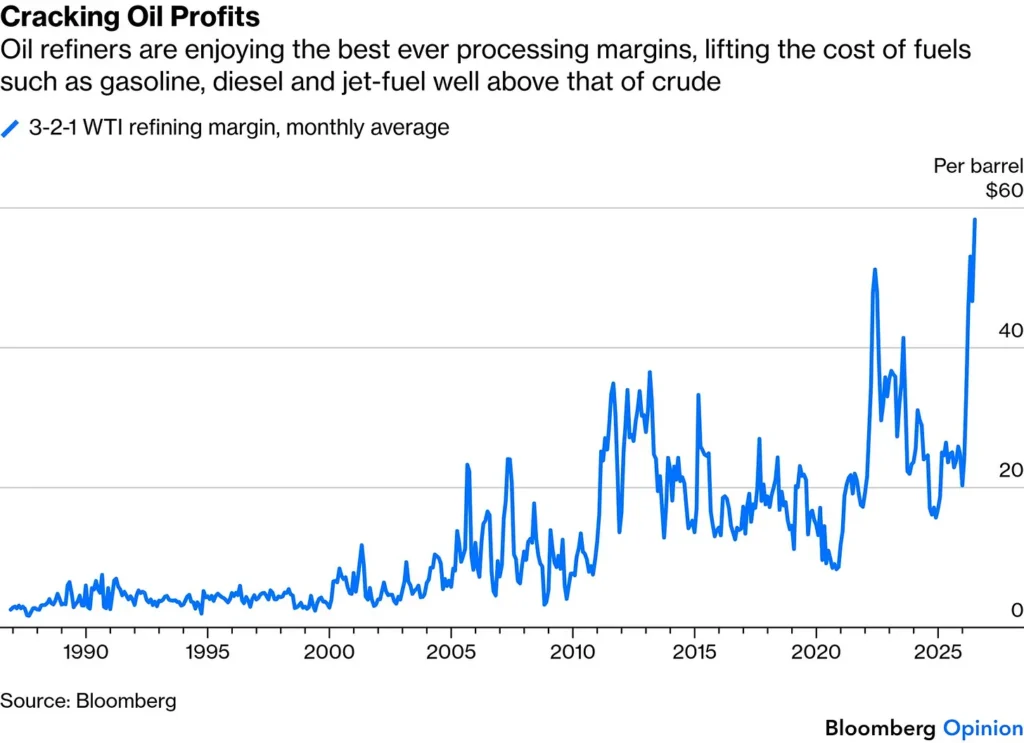

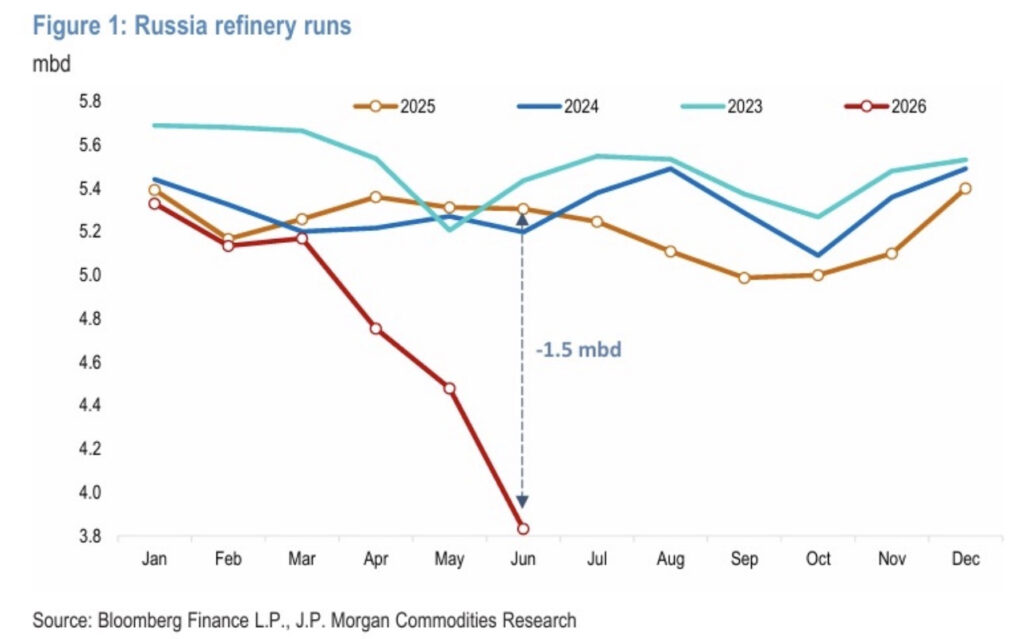

The price of oil, though, isn’t really the issue. One part of it is refinery capacity. A fair bit went off line in the Middle East, but ironically, even more in Russia. Why is Russia systematically destroying ever gas station in Ukraine? It’s retaliation for constant hits on Russian refineries.

Marathon Petroleum’s own management flagged on the Q1 earnings call that roughly 6 million barrels per day of global refining capacity is offline, about 6% of the world total. Ukraine’s drone campaign against Russian refineries is the largest single piece, but Middle Eastern facilities inside the Persian Gulf export corridor, and Chinese refiners voluntarily throttling to preserve inventory, add to the shortfall.

As a result Russia is no longer exporting diesel. And even though oil prices are low, gasoline prices are not as low as one would expect, because short refinery capacity means this:

Amusingly the Europeans and Americans have been encouraging Ukraine to hit refineries.

Now you may think “but America is an excess oil producer.”

Yeah, but it doesn’t matter. What matters is refineries and the type of crude oil involved. We aren’t just talking about gasoline, diesel, jet fuel and bunker fuel (ships), we’re talking about fertilizers, sulfuric acid (used for amazing amounts of processes) and so on. This cascades out into medicine (your aspirin for example), packaging, semiconductor production (hey, even higher prices) and whatnot.

But with rare exceptions (hello, China, again) most governments have not managed the actual supply situation.

In a rational economy prices and supply of crucial goods would be managed. For example farmers would get fertilizer and diesel at subsidized prices. Truckers shipping important goods would get subsidized diesel. Drug manufacturers would get guarnteed supplies (though not subsidized in most cases, they make tons of profits, just force them not raise prices.)

Rational governments would say “OK, what parts of the economy are actualy important (food, medicine, transport)?” and act to protect those parts of the economy, and would ration and subsidize those goods.

Instead our elites manipulate the price numbers and make the actual physical situation worse as they do so, by not allowing high prices to lower use and by not allocating key parts of the economy what they need at reasonable prices. Oh, and by releasing absurd amounts from the reserve to manipulate prices rather than using the reserve for actual necessities. They’re so used to an economy where just manipulating prices seems like all you need to do because there’s a global market with surplus. They don’t know how to handle an economy with actual, genuine shortages.

Anyway, as best I can tell if the Strait stays closed we are now weeks to about two months away from actual physical shortages in the first world. (They’ve already hit in the developing world.)

Then the fall harvest comes in and we get terrible numbers from that, and food prices surge.

This is the stupidest war of my entire lifetime and I’m old enough that this includes Vietnam, which was stupid beyond belief, but not one-tenth as moronic as the Iran war. A war of complete choice which the US has lost, won’t admit it has lost and is in danger of running the world into a decade long depression.

If it stops now or soon, it will suck, but we’ll get thru. But if Trump dismantles Iranian infrastructure like he’s threatened (by no means sure, this is Trump, but also not impossible, this is Trump) the Iranians have said they will respond by dismantling Gulf infrastructure: that means refineries that will take years and years to rebuild. Oil fields. Facilities producing helium. A decade of not enough fertilizer.

There is a real goddamn economy and if this happens, a lot of people will DIE due to famines and fuel shortages. Tens of millions. Maybe much more. You can’t just take 20 to 30% of the world’s supply of key resources offline and think “it’ll all be OK, the market will sort it out.”

I mean, the market will, sort of. But along the way will be a LOT of deaths and suffering

If the US had an even remotely operational governing system Trump would be impeached and removed in record time. He’s a fiasco, and he’s one itchy trigger finger away from being a catastrophe.

What I write here is for the benefit of everyone, but alas, I live in capitalism and I, and the site, take money to keep running. If you value the writing here and can, please subscribe or donate.

There’s book from the 2000’s called “

There’s book from the 2000’s called “

Every once in a while a complete tool graces the comments and inspires a post with their sheer stupidity.

Every once in a while a complete tool graces the comments and inspires a post with their sheer stupidity.