(Keyboard fixed, at least for now, so let’s get on with it.)

(Keyboard fixed, at least for now, so let’s get on with it.)

Trump has threatened blanket tariffs on multiple nations, including most of Europe, Canada and Mexico. This is an effective threat. The Bank of Canada estimated the effect of such tariffs on Canada at six percent of GDP, and I’ve seen an estimate for Germany of about one percent of GDP, after previous losses due to anti-Russia sanction effects on energy costs.

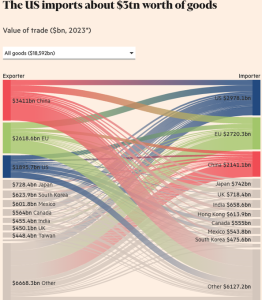

But what this tells us is that many nations are over-dependent on trade with America. Our economies are too intertwined with America’s economy, especially Canada’s. America’s massive and persistent trade deficits also indicate that America isn’t competitive. This isn’t a surprise, the American economy is controlled by oligopolies and monopolies with middlemen taking unearned profits and the overall cost structure, from housing to medical care to everything else is high, especially with respect to asset prices, which have been deliberately inflated since about 1979.

What we should do, all of us who are being threatened, is tell the US to fuck itself, slap retaliatory tariffs on the US, add in export tariffs so the US really hurts, and reorient trade towards each other—form a trade bloc without the US.

It’s worth pointing out that many of Trump’s tariffs are essentially illegal under various trade agreements the US has signed. Yet no one doubts that Trump can impose these tariffs despite their illegality. Remember that a signed treaty has the force of law in the US.

The US is, and has been a rogue nation for a long time and the rule of law means nothing in America.

I’m going to talk primarily about Canada because I know the situation here best. We’ll start with a little history.

For most of Canadian history, we exported mostly raw and refined resources to America. Minerals, oil, fish, lumber and so on. Often it was illegal to export them without doing at least primary processing: no raw logs, fish were canned in Canada and so on.

The original sin of over-integration with the US was the US-Canada auto-pact. We got a lot of jobs and factories out of it, but it was used as leverage over us. When Canada’s world-leading aviation industry of the 50s produced a jet, the Avro Arrow, which was much better than any American jet, the US threatened to take away the auto-pact unless we ended the program. And by end, I mean we disbanded Avro and we sunk the jets in a lake. Male engineers were hired by US firms, the female engineers got to be housewives, since the US in the 50s was 100% a patriarchal society. (As an aside, this was a post-war thing, the 30s were not as patriarchal.)

This story is so flaming hot in Canada that the original classification was renewed when it was due to end. Even now Canadians are angry about the Avro Arrow, something which happened 7 decades ago.

In the 80s, Prime Minister Brian Mulroney wanted a free trade pact with the US to ensure market access. Most Canadians were against it and the 88 election was fought about the FTA. Mulroney won because the anti-FTA vote was split between the Liberal and NDP parties. He rammed thru the FTA, which was later rolled into NAFTA and is now called the USMCA.

The deal included a lot more than just trade, it had IP laws and reduced the ability of Canada to use tariffs and subsidies itself and including nasty taking laws which made it nearly impossible to regulate foreign companies in Canada. Because our nation sells so many resources, the Canadian dollar tends to fluctuate a lot. When it’s high (it was higher than the US dollar for a couple years around 2015, for example) it’s devastating to our industry.

The old policy, which started around 1880 or so was called the Canadian mixed economy. When the dollar was high because of high resource prices, we’d subsidize manufacturing. When it was low, we’d subsidize resource producers and gave generous unemployment benefits to laid off resource workers.

That policy created one of the best and most prosperous economies in world history. But the condition which allowed it was that we had strong ties to both the British Empire/Commonwealth and to the US. In the 70s, the Brits, under intense US pressure since the end of WWII had their economy basically collapse. They had to go to the IMF for help and joined the EU, which bailed them out. The result of that was that their trade became very oriented towards the EU and the Commonwealth countries were left on their own.

Without a counterweight against the US, Canada felt weak. It didn’t stop Pierre Trudeau (the current PMs father) from telling the US to suck it when necessary, he even closed the border at one point, but Mulroney didn’t have the balls and he was right that our hand had become a lot weaker.

So Mulroney rammed thru the FTA. He was repaid by the Progressive Conservative party being essentially wiped out in the next election. Canadians really didn’t want the FTA/NAFTA. But once it was in, no successor government got rid of it.

The result was that Canada lost most of its industrial base. Ironically we even lost a lot of those auto-pact jobs, as American auto companies got their pants beaten off them by Japan and South Korea.

Pre-FTA about 30% of our exports to the US were autos and auto parts, 20% were petroleum, and miscellaneous machinery was about 15%.

Fast forward to today, 30% of our exports are petroleum, 13% are automobiles (the pact), and miscellaneous machinery is about 8%.

Can you say Dutch disease? Sure you can.

We’ve become a much more one note exporter, which is why Alberta and Saskatchewan are betraying our united front. They do most of the exporting, after all.

But the larger point is general de-industrialization and over-dependence on American markets. This has become enhanced over the last 8 years as our relations with China have degraded, due to Trudeau’s stupidity and pandering to America.

If this anti-China pandering worked, if it made it so America wouldn’t pull shit like tariffs, maybe it could be justified, but all its done is hurt our relationship with a potential trade partner and counter-weight to America’s influence on our economy.

So, what to do?

To start, leave the USMCA. The US has never obeyed NAFTA or the USMCA when it didn’t want to. Back in the 00s they slapped tariffs on timber, and ignored repeated rulings against them. We should have left then, but better later than never.

Second, start rebuilding our own industrial base. We still have plenty of scientists and engineers and vibrant universities. We can still bring in more scientists and engineers if we need to. This will require tariffs and subsidies, so institute them.

Third, bribe the resource workers who will be hurt. Just straight up find a way to give them a big chunk of change.

Fourth, re-institute Canadian ownership laws which require companies to be 51% Canadian owned, including foreign subsidiaries. Have the government take an additional 10%, and promise that all dividends from that 10% will be shared with Canadian citizens as direct deposits every year. Make it clear that we are willing to trade, but that trade no longer includes the right of foreigners to buy up our economy.

Fifth, form trade deals with countries other than the US. These should be bilateral or small multilateral in most cases with tariffs and subsidies allowed on both sides for key industries. We should pick a few industry sectors to concentrate on, and trade with other countries in the other sectors: that way they get something in exchange for the deal.

Sixth, go back to the old cyclical subsidization system: industry when our currency is high, resources when it’s low. Make it so that ordinary workers (and voters) are protected from the cyclical effects of a dual economy.

Seventh, put a lot of the resource profits into a sovereign wealth fund, to reduce the cyclical effects and provide the inevitable busts and for the inevitable and ongoing movement away from petrochemicals. Like it or not, alternative energy is coming on strong and the days of the petrol economy are drawing down. We’ve still got a couple decades to go, but the role of government is to make these long term plans. The fund should prioritize investments in petroleum regions, both to get them onside and to prepare them for the drawdown.

There’s plenty more details, of course, but these are the fundamentals. We’ll talk more, soon, about how trade should actually work if it’s to be for the benefit of all countries. Needless to say, such a regime would have princicples almost directly in opposition to those that have existed under GATT and its successor, the WTO.

This blog runs on donations and subscriptions from readers. It’s free, but not free to produce. If you value it, please give.

The final part of the economy is what you can get from other nations. Call this the external economy. Does someone else make it, will they sell it to you, can you afford it? Most of the time countries won’t sell other countries nukes, for example, and for much of history countries tried not to sell other countries the knowledge required to make advanced techs. When they didn’t prevent this, they paid big time: Britain was de-facto subjugated by America and America is now losing its Empire.

The final part of the economy is what you can get from other nations. Call this the external economy. Does someone else make it, will they sell it to you, can you afford it? Most of the time countries won’t sell other countries nukes, for example, and for much of history countries tried not to sell other countries the knowledge required to make advanced techs. When they didn’t prevent this, they paid big time: Britain was de-facto subjugated by America and America is now losing its Empire.