Martin Wolf, one of the best economics commenters, notes that the widespread idea that central banks, over the past 30 years, had found the holy grail of policy in inflation targeting, was clearly wrong. That’s good as far as it goes, and he’s right. But it’s worth taking farther—the problems with inflation targeting included the definition of inflation, the inflation target and the uncontrolled flow of money

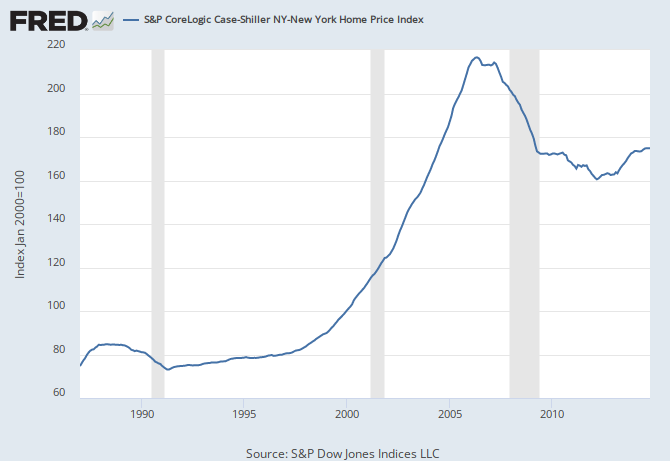

Inflation as measured during this period did not take into account asset bubbles. Wolf almost notices this, when he notes that the Fed didn’t see it as its job to stop asset bubbles. But he doesn’t go quite far enough: asset price increases are a type of inflation. If it costs more to buy a dollar of future income, a house, or a share in a company, that’s inflation. To manage inflation properly, as a central bank, requires first to know what inflation is, and that means adding asset inflation into an inflation index. This would be the opposite of the current “core inflation” index, which is non-asset inflation minus food and energy prices, ostensibly to remove volatility (which is not the way to remove volatility, the way to remove volatility is to use a moving average.) Of course, in the real world, increases in fuel prices and energy prices are, well, inflation. Add in credit price increases as well, and you’d have a measure which actually measures inflation. Target that, and you’d be targeting something real.

The second issue is simpler, the inflation target was too low. It seems like inflation being low is nothing but good, but in fact the lower it is, the more sectors of the economy are actually in deflation at any given time. If inflation is 5% and consumer goods, say, are 4% less than that, they aren’t in deflation. If inflation is at 3% and consumer goods are at 4% less, they’re at -1% and are deflating. As the last little while (and the Great Depression) have taught us, deflation is not a good thing, and yet for a long time large parts of the economy have been in and out of deflation fairly constantly. In addition, a higher rate of inflation discounts past economic activity, which isn’t an entirely bad thing, as it means people have to be agressive with their money. In a world where fraud and financial speculation wasn’t the best way to make returns, that is a good thing. (In our world, perhaps not, admittedly.)

Finally, open financial flows turn bank policies into something of a joke. As Wolf himself notes, foreign central bank independence from the Fed was largely chimerical: other central banks had to lower interest rates along with the Fed, and if they didn’t, then hot money would pour in from the US, or for that matter, from Japan, which was running its interest at zero or near zero for much of the past 20 years.

As a result, the effective interest rate was whatever the lowest interest rate of a large credible central bank with relatively stable currency was. (If you’re borrowing from a country with an unstable currency, and the currency appreciates suddenly, your apparent low interest rate can turn into a trap which costs you greatly.)

This meant that even if central banks wanted money to be expensive, for those people and corprorations able to borrow from foreign sources, it wasn’t, and the asset bubbles, inflation and so on which came from that came even if the bank was trying to be conservative. Real independent monetary policy is greatly damaged by free money flows between countries, which is even before you get to its damaging effect on real free trade and comparative advantage.

And old management maxim is that you get what you measure. Central banks weren’t measuring all inflation, and so they weren’t managing asset inflation, which is one main reason we got asset bubbles. Add to that that even where they were targetting inflation, they were targetting it at too low a level and that international money flows made it difficult to run an independent bank policy even in countries which might have wanted to, and you had a very flawed central banking system in virtually every country in the world.

So it’s not clear to me that inflation targetting is necessarily a bad policy. It seems more likely that it might have been a good policy, implemented in a very bad way. It disciplined the small actors in the economy, small businesses and ordinary workers—restricting their wages and their goods inflation, while allowing rampant inflation in securities and real-estate and (in the 90s) stocks.

The people who weren’t disciplined, then, drove a truck through the hole created and caused a disaster. The lesson isn’t “we shouldn’t target inflation”, the lesson is “we need to target all inflation” not just inflation which effects some people.

{kind=link}