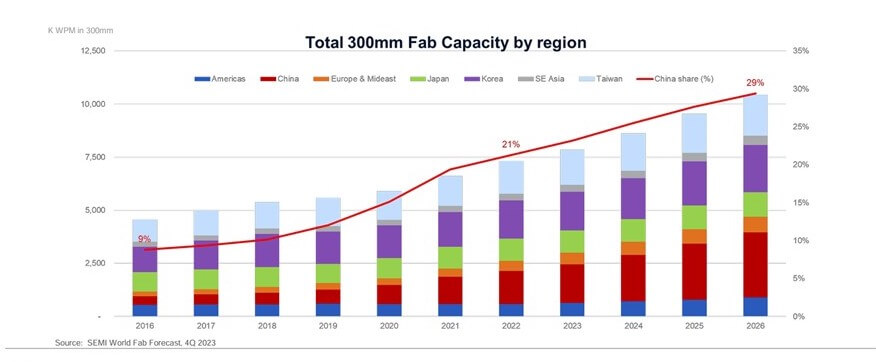

According to SEMI’s market research group, China isn’t slowing down. SEMI is forecasting China’s capacity to keep growing at a significant rate over the next few years. For 300mm, SEMI expects China to have 29% of the worldwide capacity in 2026, increasing from 21% in 2022 (Figure 2). The 200mm capacity is expected to grow from 16% to 24%. And foundry capacity is expected to reach 42% in 2026 up from 27% in 2022, outpacing the Taiwan foundry capacity expansions.

China has its goal set on being more chip-independent and spending less than $300 billion a year on importing semiconductors. To accomplish these goals, they are spending a lot of money on fabs and equipment, and in some cases forming JVs to get the right chips for their industries. So, will the European and US CHIPS Acts help to increase Europe’s and the US’s capacity? A little, but as Peter Wennink recently commented, the EU chip goal is unrealistic. I’ll add in as is the CHIPS Act in the US. China has a significant head start and it will take significant investment by the EU and US to catch up, and it is unlikely politicians and shareholders will continue to fund the exercise to reach the desired goal of 20%. (my bold)

The chart:

The bad news for equipment companies outside of China is that due to sanctions against foreign companies selling certain types of equipment, as well as China trying to create an independent chip market, Chinese semiconductor equipment companies are seeing above-market growth. Naura Technology, AMEC, and ACM Research at mid-year of 2023 are seeing 68%, 27%, and 47% growth respectively over 2022. Most of this is driven by the China market.

The Chinese, pre-sanctions, were not pushing indigenous chip capacity. Chinese companies preferred American, Taiwanese and US chips, seeing them as more reliable than domestic alternatives.

A chip act might have made sense IF the US was genuinely going to re-shore production, far beyond chips or IF it was going to go to war within the next two to three years.

As it is, all it will accomplish in the end is losing the Western absolute advantage in chips and transferring the market leading position to China.

Which brings us to this beautiful, semi-related bit of news:

This is great news. Daleep has already helped this Administration navigate some tough challenges, and there’s no kinder or more capable colleague. https://t.co/6OiywjPuA9

— Bharat Ramamurti (@BharatRamamurti) February 16, 2024

The effect of anti-Russia sanctions was to make Russia into the world’s fifth largest economy while massively ramping up their weapons production and overall growth rate. Germany has slipped to sixth and Russia is now a firm Chinese ally. It is true that America is making more money by supplying Europe with expensive fossil fuels, but by any rational assessment, anti-Russia sanctions strengthened America’s self-declared enemies, and weakened its allies.

In other words, the policy that Daleep was the architect of was a disaster. Yet he is lauded as capable rather than as a complete fuckup. To be fair, I suppose, he was undoubtedly following orders, but he owns the orders he follows unless he objected to them and predicted their failure.

All of this applies, times ten, to anyone involved in the anti-China sanctions, which have backfired catastrophically.

America, land of the highly paid incompetent fuck up.

You get what you support. If you like my writing, please SUBSCRIBE OR DONATE